Allahabad HC Quashes GST ITC Block Order for Absence of ‘Reason to Believe | Biz Flow Kit

The Allahabad High Court has overturned an order that blocked a taxpayer’s input tax credit. The court ruled that the actions taken by the GST authorities under Rule 86A of the CGST Rules, 2017, cannot be justified without a documented “reason to believe” supported by tangible evidence.

The bench of Justice Saumitra Dayal Singh and Justice Swarupama Chaturvedi has observed that the reason mentioned for blocking the ITC was a vague reference citing “as per recommendation of Superintendent (AE), Mirzapur,” which shows the absence of independent application of mind by the competent authority. It outlined that this mechanical reliance on subordinate suggestions does not fulfil the statutory limit needed under Rule 86A.

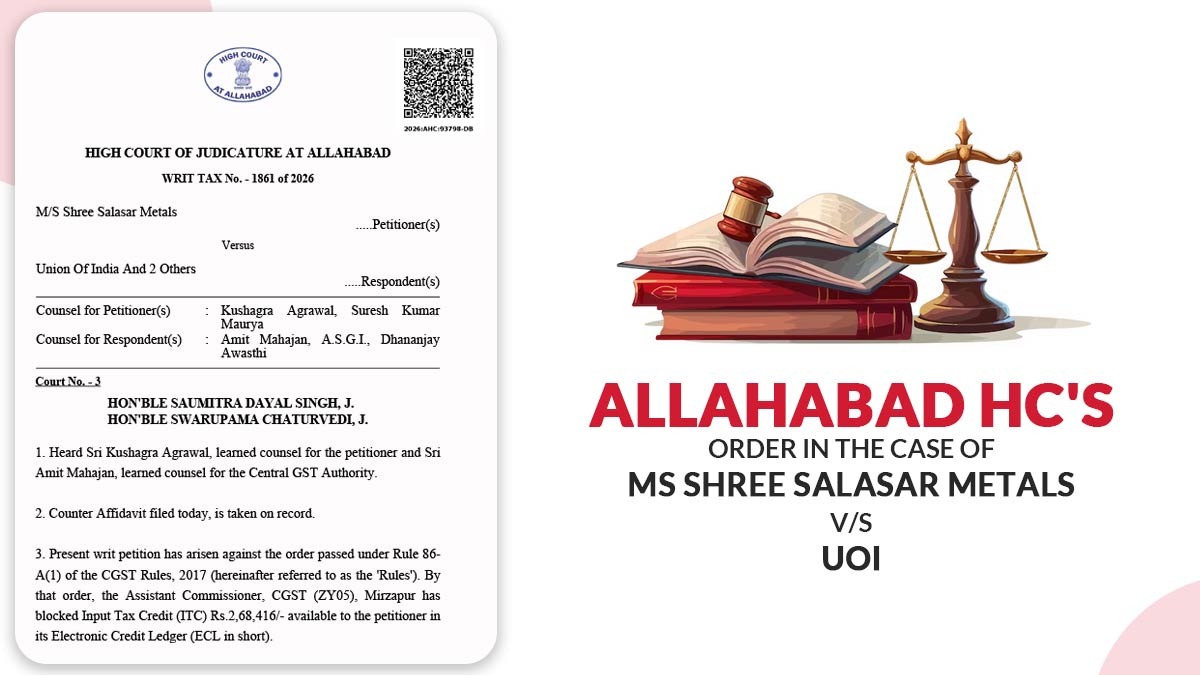

The blocking of the ITC of Rs 2,68,416 in the Electronic Credit Ledger by the Assistant Commissioner, CGST, Mirzapur, has been contested by the applicant. It was claimed by the applicant that the impugned action was without jurisdiction, because no independent satisfaction or cogent reasons had been recorded via authority before invoking rule 86A.

Read Also: Delhi HC: Rule 86A Does Not Require Taxpayers to Fulfil Any Conditions to Claim GST ITC

While the GST department claimed that the action was as per the intelligence report and an alert circular issued after an investigation of one of the suppliers of the applicant. It was alleged that the supplier was engaged in doubtful transactions and that the applicant had taken the ITC as per these supplies. However, the Court determined that such general alerts and tentative findings, lacking specific links to the petitioner’s transactions, could not constitute a valid reason to believe.

The Court, relying on earlier judicial precedents along with its own decision in M/s Pilcon Infrastructure Pvt. Ltd. and Supreme Court rulings, repeated that recording of “reasons to believe” in writing is an essential precondition for invoking Rule 86A. The belief must be founded on relevant, specific, and tangible evidence that directly connects to the alleged wrongful claim of Input Tax Credit (ITC). Mere suspicion, conjecture, or borrowed conclusions are insufficient to support such an action.

The Court emphasised that blocking ITC is a serious measure that disrupts the smoother credit chain, which is essential to the GST system. Thus, strict adherence to statutory safeguards is vital. It noted that while such actions can be taken ex parte, the requirement to record proper reasoning is even more important to prevent the arbitrary exercise of power.

The failure to reveal the basis of the reason to believe deprives the taxpayer of an appropriate remedy, because it is not feasible to contest the relevance or existence of such reasons, the Bench noted. This absence of clarity erodes procedural fairness and accountability in tax administration.

Important: How GST Software Manages Invoice Matching & Reconciliation

HC quashed the impugned order blocking the ITC. However, it furnishes liberty to the GST authorities to pass a fresh order within the laws, given that appropriate reasons are recorded and due application of mind is illustrated.

| Case Title | M/S Shree Salasar Metals vs Union Of India |

| Case No. | WRIT TAX No. – 1861 of 2026 |

| For Petitioner | Kushagra Agrawal, Suresh Kumar Maurya |

| For Respondent | Amit Mahajan, A.S.G.I., Dhananjay Awasthi |

| Allahabad High Court | Read Order |