Supplementary Coaching for Classes 5–12 Attracts 18% GST | Biz Flow Kit

There is no chance of a reduction in the cost of coaching for middle or high school students because the Gujarat Authority for Advance Ruling ruling imposes 18% GST on such services under the category of ‘supplementary education’.

“The academic coaching services provided by Friends Classes, Surat to students of Standards 5 to 12 (GSEB/CBSE curriculum) are covered under ‘Education Services’ at Sr.No.30 of Notification No.11/2017-Central Tax (Rate) dated 28.06.2017, falls under Entry No.599 ( Service Code (Tariff) 999293) of Annexure to Notification No.11/2017-Central Tax (Rate) dated 28.06.2017 as ‘commercial training and coaching services’ and is liable to GST at 18 per cent (9 per cent CGST + 9 per cent SGST),” GAAR cited in its recent ruling.

Read Also: CFI Body Demands FM to Lower GST on Coaching Centres to 5% or Zero

Experts Raise Concerns Over the Interpretation

The ruling shows that a stringent interpretation of GST exemptions aligns with the principle that ambiguities favour revenue.

Although deeming coaching as only supplementary ignores its main role as an extension of formal schooling.

If it lives, this method may question the objective of exempting educational services. The department must clarify to ensure certainty and resolve ongoing disputes, especially in the educational sector.

GST Council’s Position and Industry Demands

The same ruling supports the last year’s statement of Finance Minister Nirmala Sitharaman after the GST council meeting, suggesting overall rates. FM stated that, as coaching and other similar commercial training centres are not considered as educational institutions, therefore 18% tax rate should be applicable to them.

The Coaching Federation of India (CFI), earlier this year, in its pre-budget submission, asked to lessen GST on coaching services to 5% or NIL (complete exemption), citing that coaching institutes have limited scope to offset tax via ITC.

Applicant Raises Concerns Over Affordability

Meanwhile, the Surat-based applicant approached the GAAR, arguing that rising coaching costs negatively impact the quality and accessibility of education for low- and middle-income students aspiring to enter top institutions, thereby widening inequalities in educational opportunities and success.

The cost of specialised education and skill-based courses is higher, which discourages skill development efforts outside the traditional formal system for economically weaker sections. They have a strong opinion that taxes should not be applicable to any educational institutions for students up to 12th Std. all over India.

GAAR Rejects GST Exemption Claim

It was observed by GAAR that the supplementary education furnished by the applicant is neither pre-school education and education up to higher secondary school or equivalent nor education as a part of a curriculum for obtaining a qualification accredited by any law for the time being in force nor education as a part of an approved vocational education course’ and is thus not comes within the definition of ‘Educational Institution’ as defined in GST notification.

Ruling Limited in Scope but Influential in Impact

As “the exemption under Entry No.66 of the notification is available merely for ‘Educational Institutions’, the said exemption is not accessible to the applicant as it is not included under the definition of ‘Educational Institution’,” the authority cited while disposing of the application.

It may be noted that an AAR ruling is applicable to the applicant or the pertinent tax office, but many such rulings have served as a foundation for policy-making.

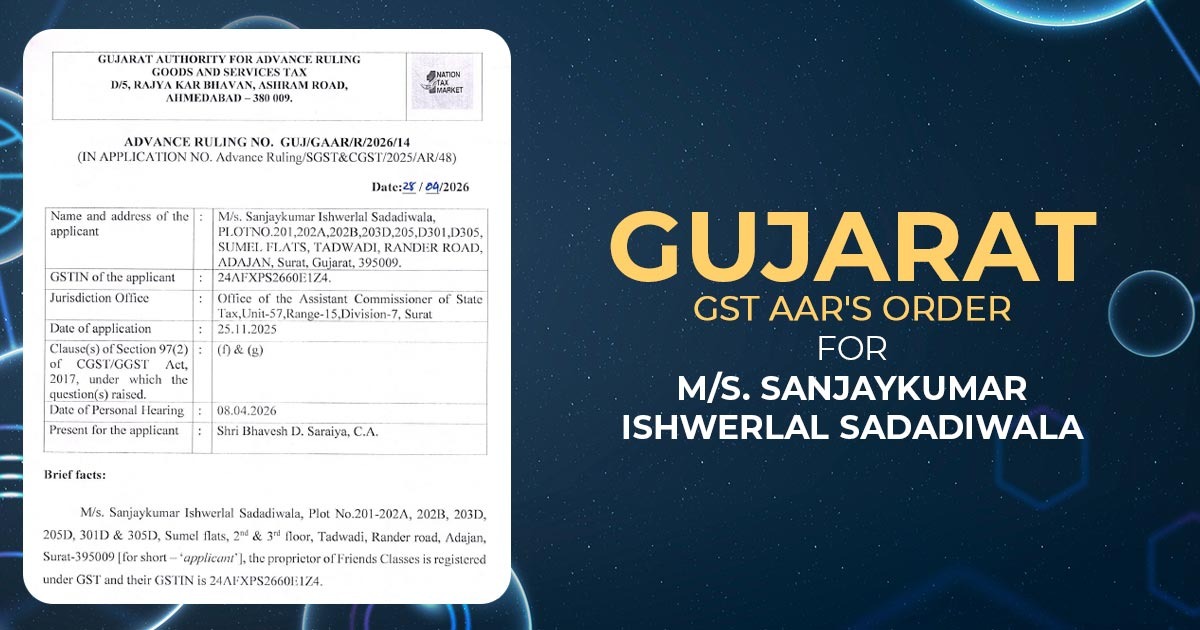

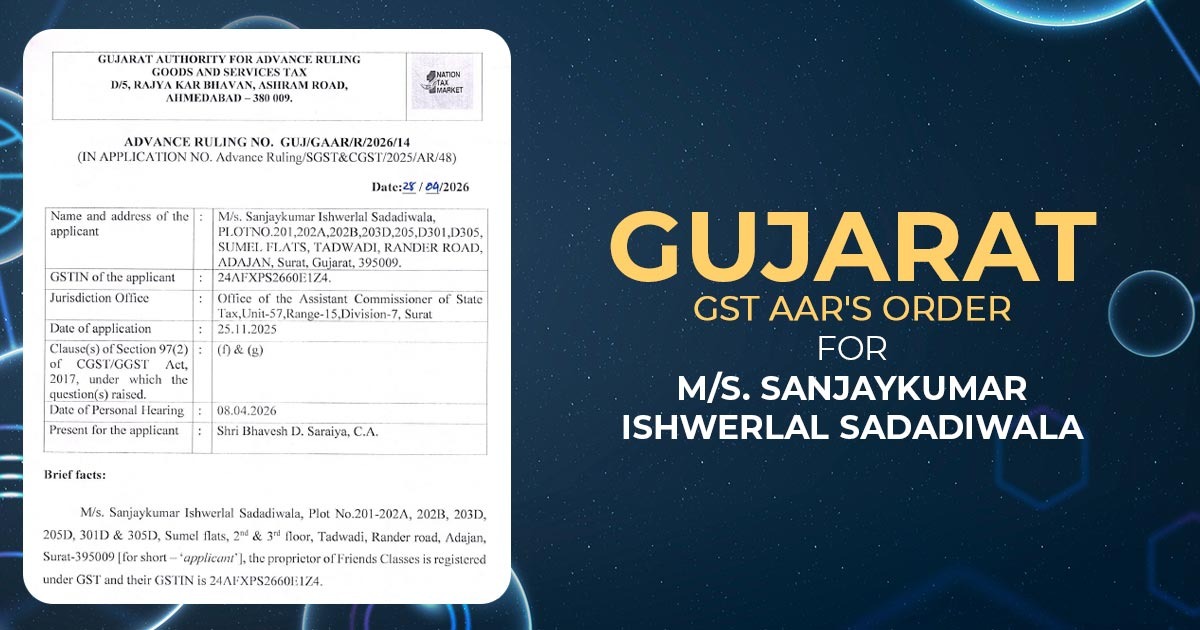

| Case Title | M/s. Sanjaykumar Ishwerlal Sadadiwala |

| GSTIN of the Applicant | 24AFXPS2660E1Z4 |

| Present for the applicant | Shri Bhavesh D. Saraiya |

| Date | 28.04.2026 |

| Gujarat GST AAR | Read Order |