Section 54 Exemption Cannot Be Denied for Non-Deposit in CGAS if Entire Capital Gain Invested Before ITR Filing | Biz Flow Kit

In a significant relief for taxpayers claiming capital gains exemption, the Mumbai Bench of the Income Tax Appellate Tribunal has held that a deduction under Section 54 of the Income Tax Act cannot be denied merely because the assessee did not deposit the amount in the Capital Gains Account Scheme (CGAS), provided the entire capital gain was invested in a new residential property before filing the income tax return.

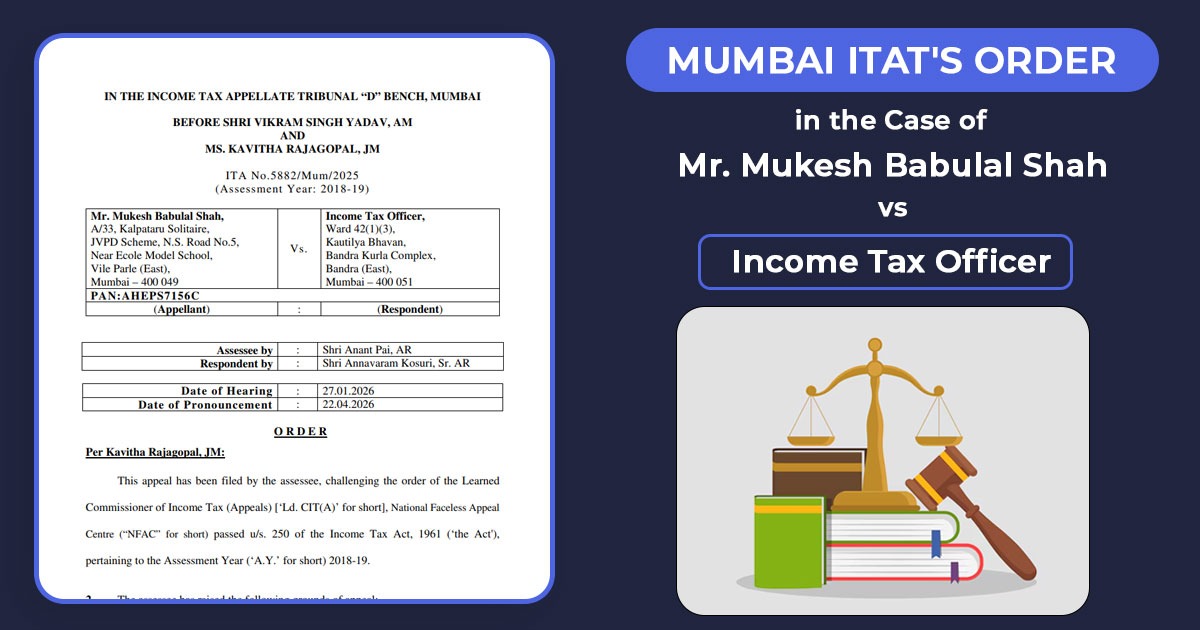

The case comprises Mukesh Babulal Shah for Assessment Year 2018-19. The taxpayer had sold multiple properties in FY 2017-18 for nearly Rs 5.03 crore and claimed an exemption of Rs 3.69 crore under s. 54 after investing in a new residential property.

The assessing officer refused the exemption on the fact that the taxpayer neither deposited the unused capital gains in the Capital Gains Account Scheme before the deadline u/s 139(1) nor completed the investment within the specified duration. The first appellate authority upheld the addition.

The taxpayer before the Tribunal claimed that although the return was submitted with a delay u/s 139(4), the capital gain had already been used to purchase a new property before filing the return, leaving no unused amount requiring deposit under the scheme.

In the case of Humayun Suleman Merchant, the revenue relied on the Bombay High Court ruling, claiming that the deposit in the notified account before the deadline u/s 139(1) was obligatory.

Read Also: Important Steps for Beginners to Filing Income Tax Return

But, concerning the present matter, the Tribunal distinguished the facts. It stated that the taxpayer had allegedly invested the complete amount in the new property dated 24 December 2018 before filing the return, though the sale agreement was implemented afterwards on 31 January 2019.

The bench said that the Bombay High Court had considered the norms specified by the Gauhati High Court in Rajesh Kumar Jalan, where exemption was granted if the capital gains were wholly used before return filing u/s 139, including a belated return u/s 139(4).

Subsequently, the Tribunal maintains that where unused capital gains remain as on the return filing date, the provision of depositing funds in the capital gains account scheme shall not be applicable.

Therefore, the Tribunal decided that if no unused capital gain was left when the return was filed, depositing funds into the Capital Gains Account Scheme was not necessary.

The case was remanded back to the assessing officer for verification of the new property payments. The tribunal, as per these verifications, asked the department to permit the section 54 deduction claim.

| Case Title | Mr Mukesh Babulal Shah vs. Income Tax Officer |

| Case No. | ITA No.5882/Mum/2025 |

| Assessee by | Shri Anant Pai |

| Respondent by | Shri Annavaram Kosuri |

| Mumbai ITAT | Read Order |

![Finance Ministry Notifies Additional India-Bhutan Land Customs Route at Samrang [Read Notification]](https://bizflowkit.in/wp-content/uploads/2026/05/CBIC-Notifies-Additional-India-Bhutan-Land-Customs-Route-at-Samrang-768x432.jpg)