Karnataka AAR Backs Margin-Based GST on Used Vehicle Sales | Biz Flow Kit

The Karnataka Authority for Advance Ruling (AAR) has held that while the margin scheme is not specified under the GST law, taxation based on margin can be applied subject to strict compliance with the prescribed conditions.

The bench of Kalyanam Rajesh Rama Rao and Sivakumar S Itagi has mentioned that second-hand motor vehicles fall under Heading 8703 of the GST Tariff, which includes vehicles designed for passenger transport.

The applicant had approached the AAR for clarity on GST implications for a business model comprising the purchase of second-hand cars from unregistered sellers, carrying out minor repairs, and reselling them to customers. Also, the applicant mentioned that the annual turnover seems to surpass 40 lakh, triggering GST registration pre-requisites.

The main issue before the authority was whether GST can be charged on the margin (difference between purchase and sale price) for the case of second-hand car transactions, and under what conditions such a benefit could be taken.

As per the authority, although the term margin scheme is mentioned under the CGST Act, the valuation procedure for second-hand goods is furnished under Rule 32(5) of the CGST Rules, 2017.

According to this rule, GST is applicable on the difference between the selling price and the purchase price of used goods. This benefit is available only if no input tax credit (ITC) has been claimed on the purchase. If the margin is negative, it should be disregarded for tax purposes.

The AAR also noted that Notification No. 8/2018-Central Tax (Rate) specifically supports this principle for old and used motor vehicles.

Even after furnishing various chances, the applicant did not provide the necessary documentation, which is an important factor in the case. The authority had asked for the information on the transfer of ownership at the purchase and sale stages, supporting documents evidencing such transfers, and accounting treatment of vehicles.

Read Also: How GST Software Handles Notices & Hearings Easily U/S 73

Petitioner did not appear for the subsequent hearings nor furnish the required clarifications. This restricts the ability of the authority to conclusively determine eligibility for the benefit.

Because of inadequate information on engine capacity, Vehicle length, and Fuel type, the Authority abstained from determining the GST rate applicable in the case.

The Karnataka AAR determined that the concept of the margin scheme is not described in the GST law. However, valuation under Rule 32(5) is applicable to second-hand goods, including used cars, as long as certain conditions are fulfilled.

GST is liable to be paid on the margin, which is the difference between the selling price and the purchase price, provided that no Input Tax Credit (ITC) is claimed and the conditions of Notification No. 8/2018 are fulfilled. Motor vehicles fall under Heading 8703, but the specific GST rate could not be determined due to insufficient details.

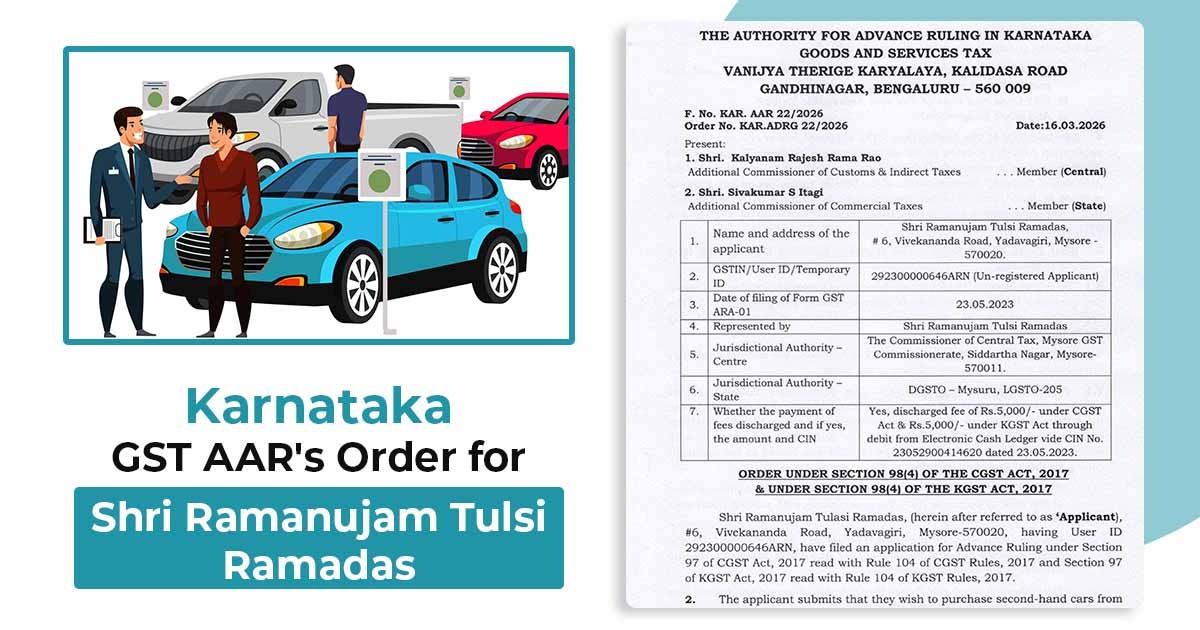

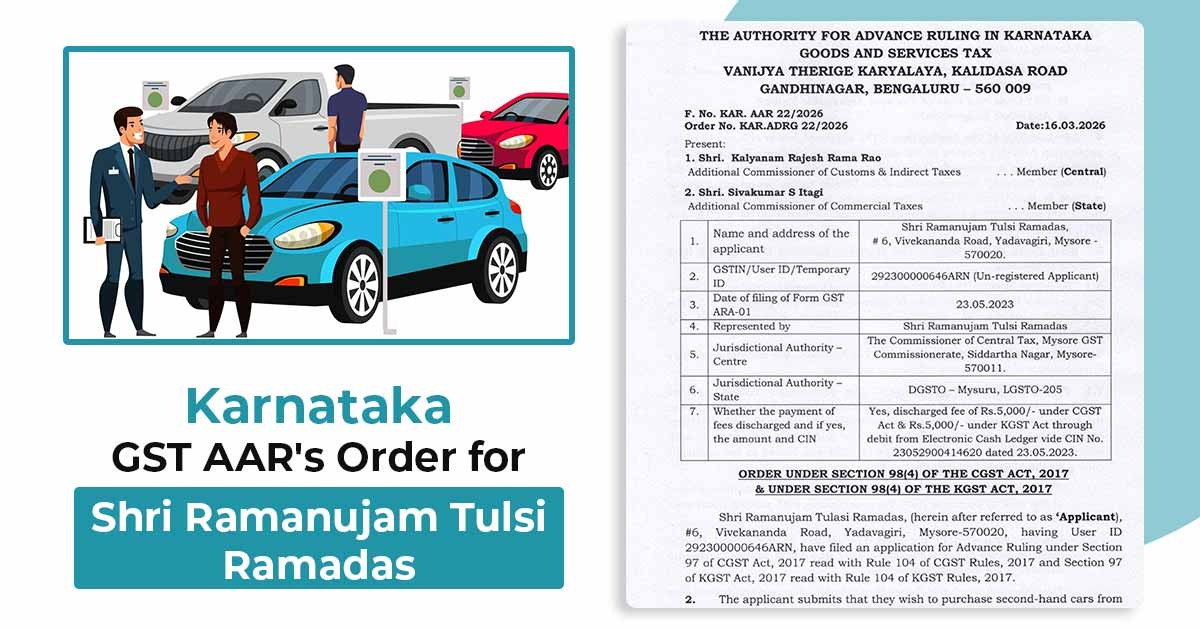

| Case Title | Shri Ramanujam Tulsi Ramadas |

| Oder No. | KAR.ADRG 22/2026 |

| Date: | 16.03.2026 |

| GSTIN/User ID/Temporary ID | 292300000646ARN (Un-registered Applicant) |

| Karnataka AAR | Read Order |