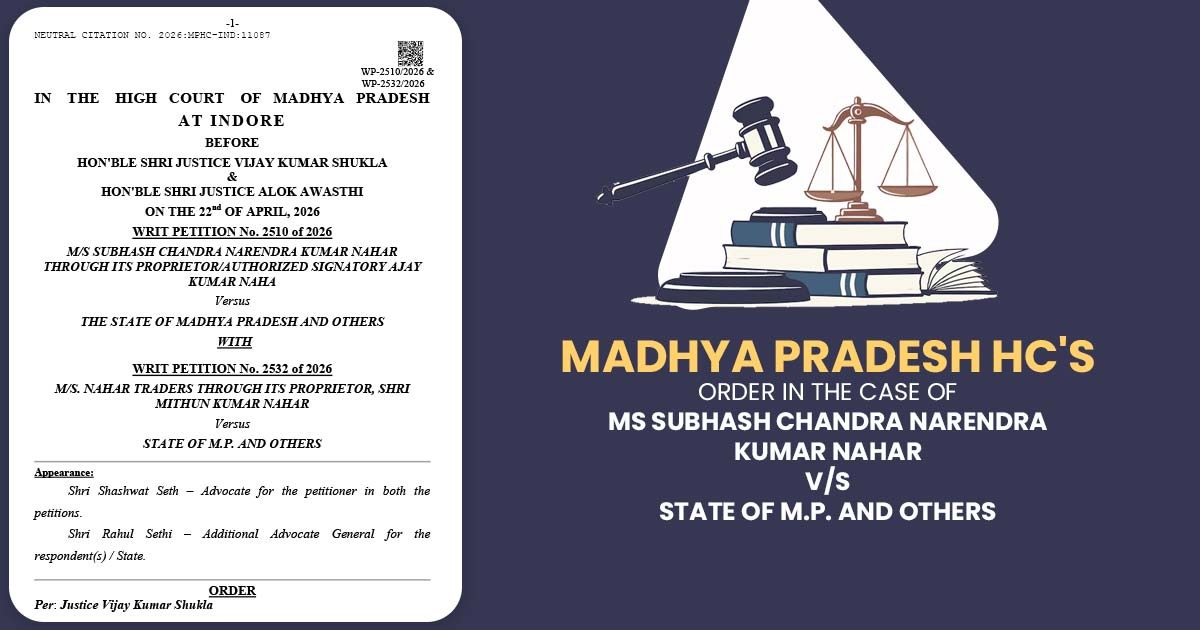

MP HC Quashes ₹7 Crore GST Demand, Rules Assistant Commissioner Not a Proper Officer Without Council Nod | Biz Flow Kit

In a massive relief for the taxpayers involved, the Madhya Pradesh High Court recently stepped in and completely quashed a massive demand order of over 7 crore. The court firmly held that an Assistant Commissioner simply cannot take on the role of a Proper Officer if there is no valid recommendation provided by the GST Council to back them up.

The division Bench, which consisted of Justice Vijay Kumar Shukla and Justice Alok Awasthi, made a very important observation regarding this matter. They noted that the whole concept of a Proper Officer isn’t just some basic procedural formality; it actually goes straight to the very root of jurisdiction itself.

The judges made it clear that the authorisation of State officers to act as Proper Officers needs to strictly follow the statutory requirements. This includes following the specific conditions laid out under Section 6 of the UTGST Act. Without a proper and valid recommendation coming from the GST Council, you just can’t presume that such authorisation exists.

To give some background on the case, the impugned order in question was originally passed by the Assistant Commissioner of State Tax (Anti-Evasion Bureau), Indore. This order ended up creating a huge tax demand of exactly 7,01,61,092 against the petitioners.

These legal proceedings actually started because of a deep investigation into the alleged wrongful availment and passing on of Input Tax Credit (ITC). The tax department was alleging that a certain supplier entity had wrongfully availed ITC without even bothering to actually deposit the required tax with the Government. After doing that, they supposedly passed on this credit down the line through a complex chain of transactions.

As a direct result of all this, the petitioners, who were just the recipients in this scenario, were held accountable. They were accused of violating the strict mandatory conditions mentioned under Section 16(2)(b) and 16(2)(c) of the Central Goods and Services Tax Act, 2017. However, the core challenge that the petitioners raised during the trial was quite interesting. They strongly argued that the Assistant Commissioner who actually passed the order was not even the Proper Officer as it is defined under Section 2(91) of the CGST Act.

They essentially argued that this specific officer completely lacked the necessary jurisdiction to even adjudicate the matter in the first place. According to the department’s own internal administrative orders, the powers for adjudication were supposed to be distributed based on specific turnover thresholds. So, for business entities that have a much higher turnover, only a Deputy Commissioner was legally authorised to pass such heavy orders.

Because of this massive flaw, it was contended that the impugned order was totally void ab initio simply for the want of jurisdiction. Naturally, the State tried to defend the order. They did this by invoking Section 6 of the Union Territory Goods and Services Tax Act, 2017. This specific section does permit State tax officers to function as Proper Officers, but only under certain strict conditions.

But here is where things went downhill for the State. During the actual course of the hearing, the Court specifically asked them if there had been any actual recommendation made by the GST Council to properly authorise such an appointment. In response to this direct question, the State candidly admitted that, well, no such recommendation actually existed at all. Because of this admission, the competence of the Assistant Commissioner just couldn’t be legally justified anymore.

Important: How GST Software Fixes Common Mistakes in SCN Replies

Moving forward, the Court further reiterated a crucial legal point. They stated that just because there is an existence of an alternative remedy available under Section 107 of the CGST Act, it definitely does not bar the court from exercising its writ jurisdiction, especially in cases where the initial order was clearly passed without any jurisdiction. To support this stance, heavy reliance was placed on the famous landmark judgment in Whirlpool Corporation v. Registrar of Trademarks (1998). This older case famously permits writ intervention whenever there are glaring jurisdictional errors involved.

Wrapping things up, the Court firmly concluded that the impugned order was unfortunately passed by an incompetent authority and was therefore completely unsustainable in the eyes of the law. Ultimately, the High Court quashed the massive demand order dated December 30, 2025. However, they did grant the liberty to the actual competent authority to go ahead and pass a fresh order, as long as it is done strictly in accordance with the law. With that decided, both of the writ petitions were officially allowed and completely disposed of.

| Case Title | MS Subhash Chandra Narendra Kumar Nahar Versus State Of M.P. And Others |

| Case No. | W.P.510 of 2026 |

| For Petitioner | Shri Shashwat Seth |

| For Respondent | Shri Rahul Seth |

| Madhya Pradesh High Court | Read Order |