Allahabad High Court Allows GST Appeals Before GSTAT Till June 30, 2026 | Biz Flow Kit

The Allahabad High Court has decided that taxpayer can now submit their appeals to the GST Appellate Tribunal (GSTAT) until June 30, 2026.

The bench of Justice Dr Yogendra Kumar Srivastava noted the absence of a functional GST Appellate Tribunal, refusing Statutory Right to Appeal, and disposed of a writ petition that had contested the absence of a Tribunal u/s 109 of the Central Goods and Services Tax (CGST) Act, 2017.

The applicant said it was not given its statutory rights to contest orders passed under Sections 107 and 108 of the CGST Act because of the non-constitution of the GST Appellate Tribunal.

The State authorities at the time of proceedings notified the Court that the Central Government had chosen the measures for operationalising the Tribunal. On September 24, 2025, the GST Appellate Tribunal was formed, and members were appointed via an office order on December 26, 2025, with directions to assume charge by January 21, 2026. Also, procedural norms controlling the operations of the Tribunal had earlier been reported dated April 24, 2025.

Before the court, it was also furnished that the Central Government, in exercise of powers under section 112(1) of the CGST Act, had issued a notification on September 17, 2025, stipulating June 30, 2026, as the due date for filing appeals before the Tribunal in cases where the impugned orders were communicated before April 1, 2026.

The court, considering such developments, stated that the procedure to make the GST Appellate Tribunal operational had earlier been set in motion and that continuing the writ proceedings would not serve a valuable objective. Therefore, without analysing the merits of the impugned orders, the court moved to dispose of the petition with directions securing the right to appeal of the applicant.

The applicant was furnished with a chance to submit a plea before the GST Appellate Tribunal within the extended duration ending June 30, 2026. It is directed that if the same appeal is submitted within the stipulated period, then no objection concerning limitation shall be raised by the authorities.

As per the court, any amount deposited by the applicant as per the interim directions of the HC will be considered as compliance with the statutory pre-deposit requirement u/s 112(8) of the CGST Act, subject to submission of proof along with a certified copy of the interim order.

Also Read:- Chhattisgarh HC Allows Relief in GST Recovery Case, Directs Taxpayer to Follow CBIC Circular

The Court specified procedural safeguards, requiring that any defects in the appeal be intimated by the Tribunal authorities within 3 weeks of filing, and that the applicant correct them within 30 days thereafter. It claimed that the appeal will be adjudicated on the merits and in accordance with the law.

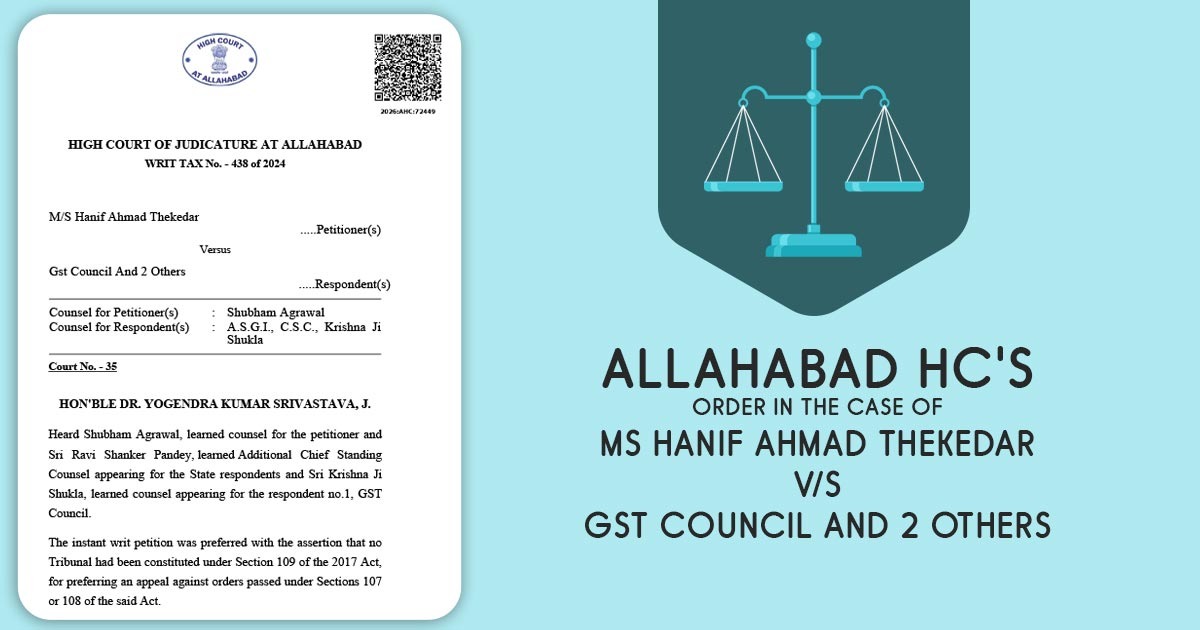

| Case Title | Ms Hanif Ahmad Thekedar V/S GST Council And 2 Others |

| Citation | WTAX No. 438 of 2024 |

| Counsel For Petitioners | Shubham Agrawal |

| Counsel For Respondents | A.S.G.I., C.S.C., Krishna Ji Shukla |

| Allahabad High Court | Read Order |

![Karnataka Govt Ends 100% Tax Exemption on EVs in State, Effective April 2026 [Read Notification]](https://bizflowkit.in/wp-content/uploads/2026/04/Tax-Exemption-on-EVs-Ends-in-Karnataka-New-Rates-Apply-From-2026-768x432.jpg)