Unsigned GST Assessment Order Held Legally Defective Can’t Be Sustained in Law | Biz Flow Kit

The Andhra Pradesh High Court on 15th June stated that an unsigned GST assessment order faces an inherent legal defect and cannot be kept in law, reaffirming that regulatory orders should have accurate authentication to be enforceable.

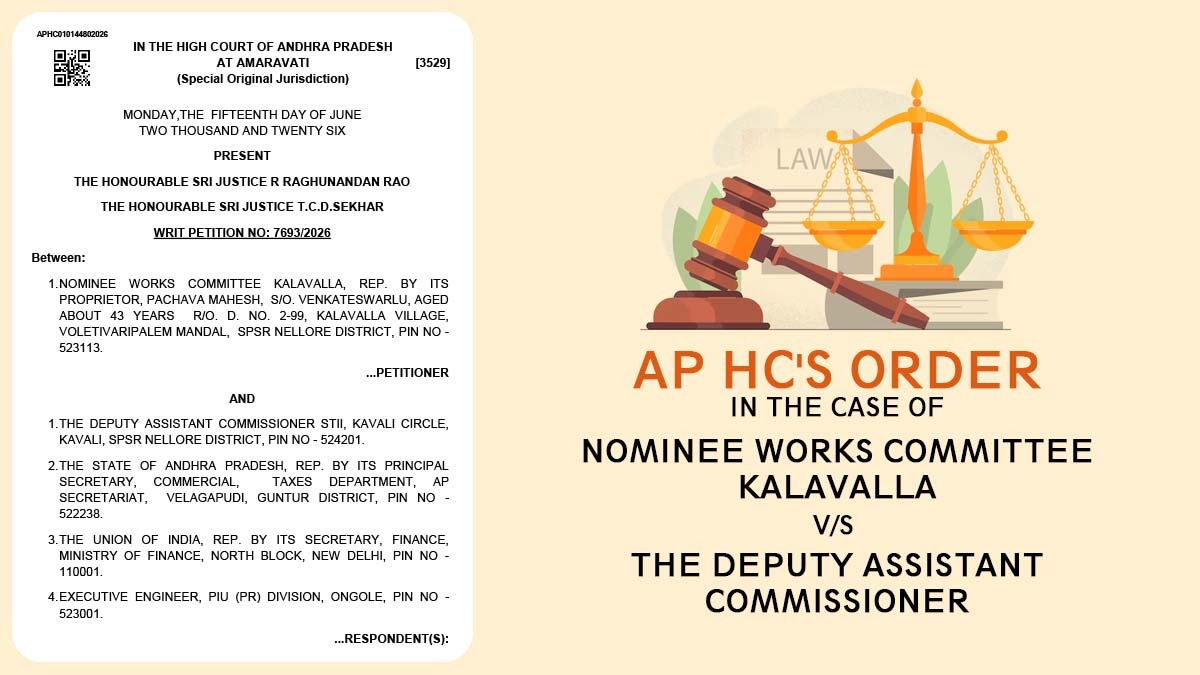

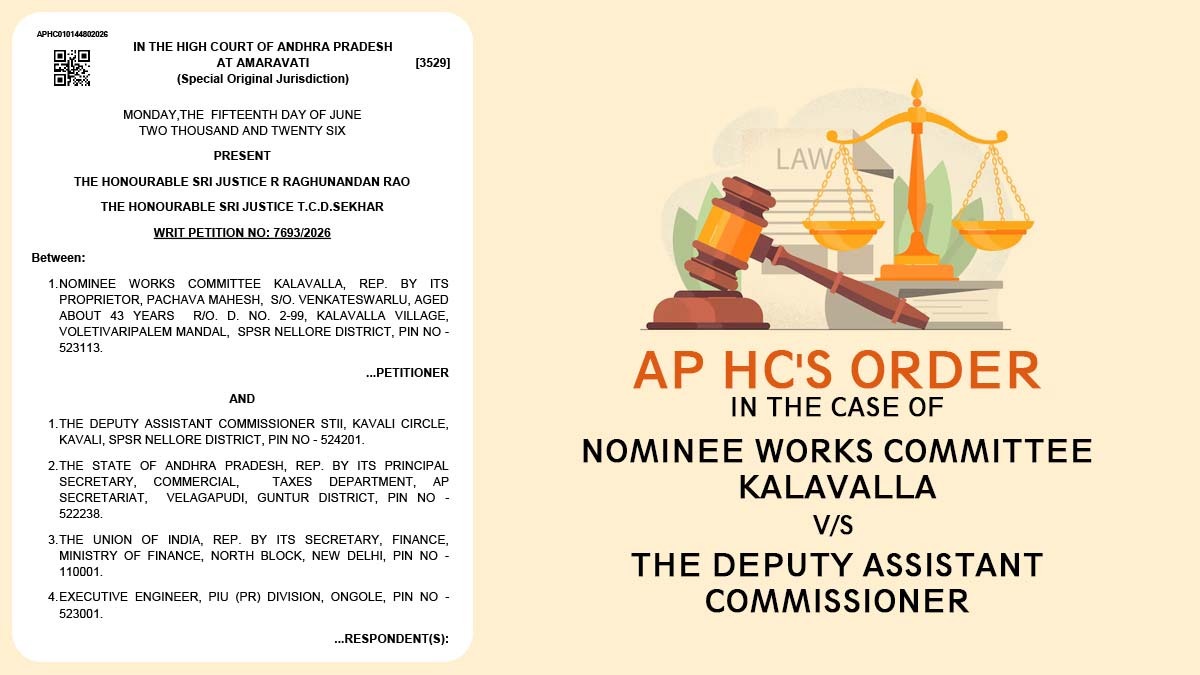

A Division Bench of Justices R. Raghunandan Rao and T.C.D. Sekhar overturned the impugned assessment order while allowing the writ petition submitted by Nominee Works Committee Kalavalla and remanded the case for fresh adjudication. The judges stated:

“This Court is also not unaware of the practical difficulties that have arisen on account of the introduction of the GST regime and the introduction of the online mechanism, under this regime, for the administration of tax collection, etc.”

Nominee Works Committee Kalavalla contested the proceedings issued in Form GST DRC-07 and the following recovery action in Form GST DRC-16. It claimed that the assessment order was not correct as it did not specify the signature of the assessing officer and was not served via conventional modes, with the department relying only on the upload of the order on the GST portal as valid service.

Meanwhile, the State said that u/s 169(1)(d) of the GST Act, uploading orders on the GST portal comprises a valid service on a registered person, and hence the challenge was belated and not maintainable.

The Court referred to previous decisions of the Andhra Pradesh High Court, which had stated that the absence of a signature on an assessment order is a substantive defect and cannot be resolved by resorting to Sections 160 and 169 of the GST Act.

It marked issues that taxpayers encounter in accessing orders uploaded on the GST portal and stated that various registered persons had approached the Court, mentioning the inability to access the portal or the absence of communication from authorised representatives.

Bench underlines that these facts may not comprise adequate cause for delay. It affirmed that systemic hardship emerging from the GST online procedure could not be overlooked, where the order itself faces a patent legal defect.

Read Also: How GST Software Helps Protect Your Business from Cancellation

It asked the applicant to deposit 20% of the disputed tax within 6 weeks, subject to adjustment of amounts earlier filed and the final consequence of the reassessment proceedings.

Subsequently, the HC affirmed the assessment order to be invalid for want of signature, overturned it, and asked for fresh adjudication, post-granting the applicant a reasonable chance of hearing.

| Case Title | Nominee Works Committee Kalavalla vs. The Deputy Assistant Commissioner |

| Case No. | Writ Petition No: 7693/2026 |

| For Petitioner | Saranu Phani Teja |

| For Respondent | GP FOR Commercial Tax |

| Andhra Pradesh High Court | Read Order |