Calcutta HC Refuses Stay on Sec. 74 SCN in Namkeen GST Case; Orders Detailed Hearing on CBIC Circular | Biz Flow Kit

The Calcutta High Court has refused to grant an interim stay on a show-cause notice issued under Section 74 of the CGST Act regarding a classification dispute over “Namkeen” products. The court noted that a thorough hearing is required to address the validity of the underlying government circular.

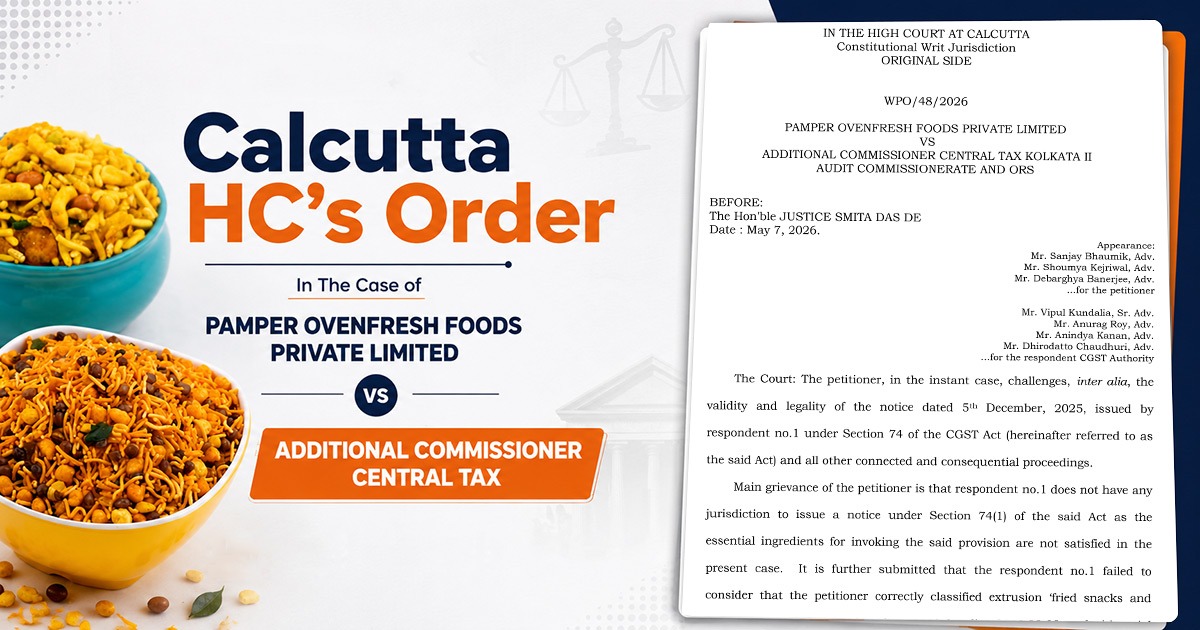

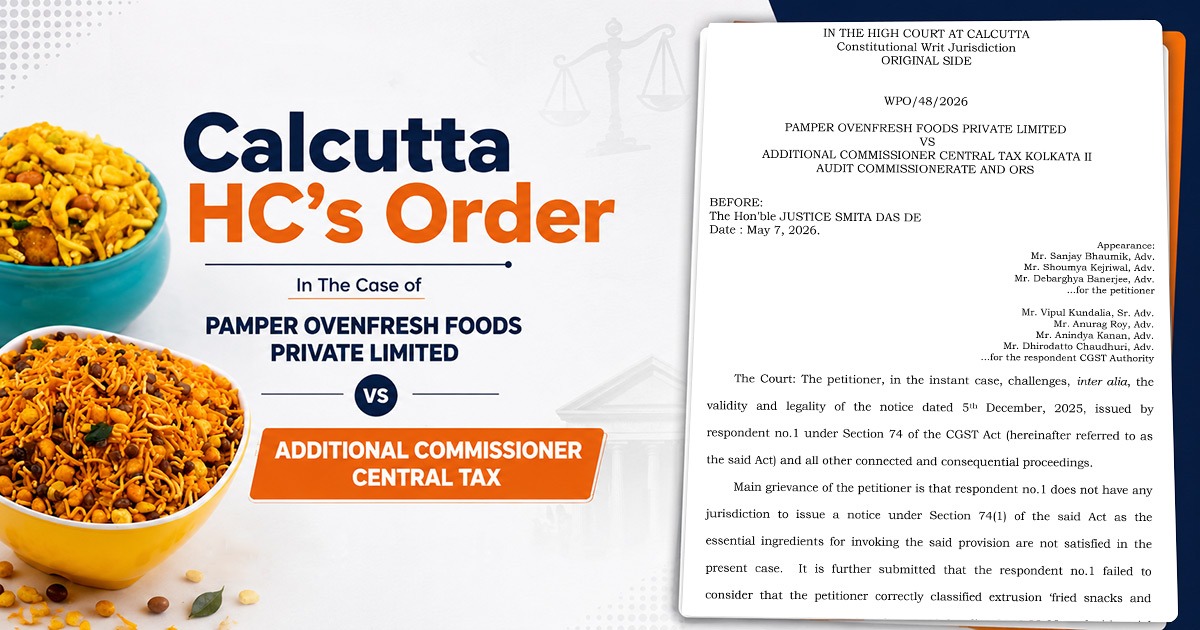

The applicant, Pamper Ovenfresh Foods Private Limited, approached the Court contesting a notice dated December 5, 2025, issued by the Additional Commissioner of Central Tax. The applicant challenged the invocation of Section 74 of the CGST Act, which is relevant to tax not paid due to fraud, wilful misstatement, or suppression of facts.

The dispute with the applicant is that respondent no.1 does not have any jurisdiction to issue a notice u/s 74(1) of the said Act, as the important ingredients for invoking the said provision are not fulfilled in the present case. It also stated that the respondent no.1 does not acknowledge that the applicant accurately categorised extrusion ‘fried snacks and pellet fried snacks’ under the relevant sub-heading 2106 90 99 read with serial no.46 of the Schedule II of the Rate Notification, and thus, Section 74 is not applicable. An issued GST SCN via the respondent no.1 u/s 73 of the said Act proposing reclassification of the product in question is cited to be without jurisdiction.

The taxpayer contended that there were no valid reasons to apply this strict provision, as they had accurately classified their products, extrusion-fried snacks and pellet-fried snacks, under sub-heading 2106 90 99, in accordance with Serial No. 46 of Schedule II of the Rate Notification. This classification attracted a 12% GST.

The applicant’s counsel argued that the Revenue Department improperly sought to reclassify the goods to impose an 18% tax rate. He referenced CBIC circulars dated January 31, 2023, and October 11, 2024, to support his claim that products like ‘Namkeen’ have consistently been considered under the tariff entry proposed by the applicant. He stated that the simultaneous issuance of an SCN u/s 73, followed by a notice u/s 74, was beyond the department’s jurisdiction.

Read Also: How GST Return Software Fixes Common Mistakes in SCN Replies

Senior Advocate Vipul Kundalia, representing the Revenue, contested the writ petition’s maintainability. He asserted that an SCN should only be challenged under exceptional circumstances. He emphasised that the applicant had initially given an undertaking on May 26, 2025, to submit a detailed response but later failed to do so, which compelled the authority to issue the notice u/s 74.

Justice Smita Das De observed that the applicant has contested the validity of the circular dated January 13, 2023, indicating the need for a “proper and extensive hearing” concerning the issue of vires. The Court concluded that no interim order was necessary at this time and directed the respondents to file an affidavit in opposition within 2 weeks following the vacation. The court scheduled the case for further hearing on June 26, 2026.

| Case Title | Pamper Ovenfresh Foods Private Limited Vs Additional Commissioner Central Tax |

| Case No. | WPO/48/2026 |

| For Petitioner | Mr. Sanjay Bhaumik, Adv. Mr. Shoumya Kejriwal, Adv. Mr. Debarghya Banerjee, Adv. |

| For Respondent | Mr. Vipul Kundalia, Sr. Adv. Mr. Anurag Roy, Adv. Mr. Anindya Kanan, Adv. Mr. Dhirodatto Chaudhuri, Adv. |

| Calcutta High Court | Read Order |