ITAT Rules Rental Receipts Still Taxable as House Property Income | Biz Flow Kit

Charging GST on Rent Doesn’t Make It Business Income: ITAT Rules Rental Receipts Still Taxable as House Property Income

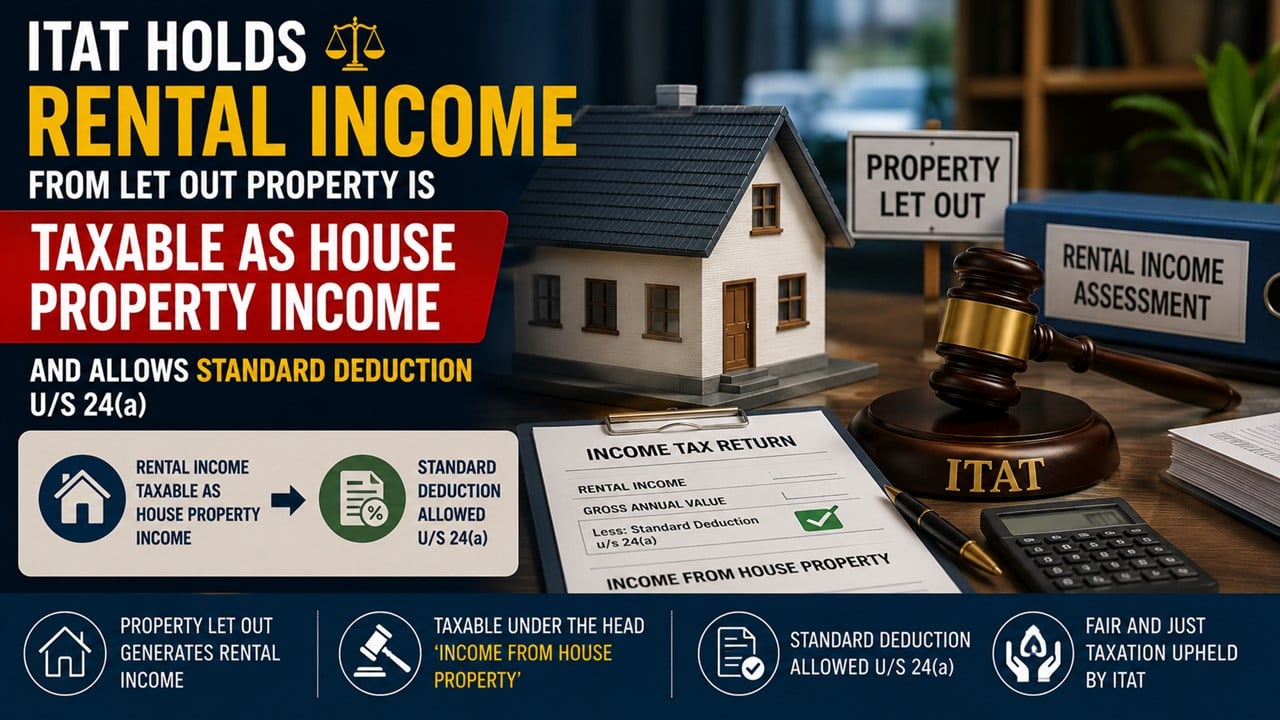

The Income Tax Appellate Tribunal (ITAT) Delhi has held that the rental income received by M/s Gogia Developers from their let-out property is taxable under the head “Income from House Property” and not as business income.

M/s Gogia Developers is a partnership firm and had not filed its return of income under Section 139 of the Income Tax Act, 1961 for assessment year 2020-21. On the basis of the information on the Insight Portal that indicated rental income amounting to Rs 20.73 lakh, the reassessment proceedings under Sections 147 and 148 were initiated. In response to the notice under Section 148, the assessee filed its return and declared the rental receipts under the head “Income from House Property” and claimed deductions under Sections 24(a) and 24(b).

During reassessment proceedings, the AO found out that the assessee had availed a loan by mortgaging the rented property and used the proceeds for purchasing another property. The AO further observed that the assessee was engaged in leasing activities and had charged GST on rent. Accordingly, he treated the rental receipts as business income and denied the standard deduction under Section 24(a) and assessed the income under the head “Profits and Gains of Business or Profession.” The CIT(A) upheld the assessment order.

The Tribunal noted that the assessee had merely let out the premises along with basic facilities and there was no intention to do any organised business activity involving the premises. The Tribunal observed that GST and Income Tax operate in different spheres and the levy of GST on rental receipts does not by itself establish that such receipts constitute business income.

Accordingly, the Tribunal held that the license fee received by the assessee was assessable under the head “Income from House Property” and that the assessee was entitled to claim the standard deduction under Section 24(a) of the Act. Consequently, the appeal was partly allowed for statistical purposes.

Join StudyCafe Membership. For More details about Membership Click Join Membership Button

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe’s WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!”