GST Cancellation Proceedings Must Be Dropped if Returns Filed and Dues Paid | Biz Flow Kit

A relief has been given by the Gauhati High Court to a registered taxpayer, Sama Yangfo

Son of Shri Gumkap Yangfo, whose GST registration was cancelled because of not filing the returns.

The applicant, Sama Yangfo, operates a business named “M/s Anney Donyi Enterprises“, registered under the Goods and Services Tax (GST) Act.

The tax department had cancelled the GST registration of the applicant as he had not filed returns for more than 6 months. An SCN was issued directing him to answer; he did not respond on time. Consequently, the Arunachal Pradesh tax authority has passed a GST order.

The applicant, before the Gauhati High Court, mentioned that he was clueless about the online process and put reliance on a tax consultant, which caused the delay. He mentioned that he cleared all due GST returns and filed the taxes, interest, and late fees. But when he attempted to restore his registration, the system rejected his request because the deadline had lapsed.

The High Court said that the proviso to sub-rule (4) of Rule 22 of the Rules of 2017 authorises authorities to cancel these proceedings if the taxpayer wants to file all the pending GST returns and make full payment of tax.

Important: Tax Return Filing Errors and How GST Software Controls Them

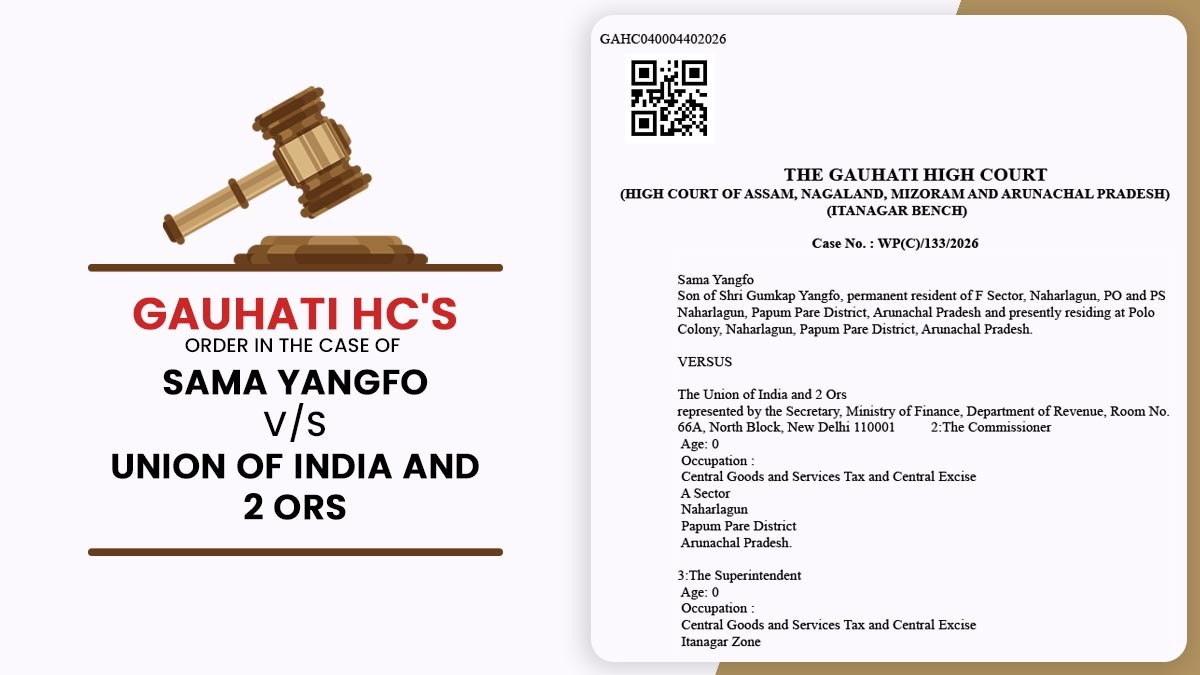

| Case Title | Sama Yangfo V/S Union of India and 2 Ors |

| Case No. | WP(C)/133/2026 |

| Counsel For Appellant | Duge Soki, T Nima,Minter Karbak |

| Counsel For Respondent | Marto Kato, SC Central Excise and Customs, Tania Kipa, DSGI |

| Gauhati High Court | Read Order |

Disclaimer:- “All the information given is from credible and authentic resources and has been published after moderation. Any change in detail or information other than fact must be considered a human error. The blog we write is to provide updated information. You can raise any query on matters related to blog content. Also, note that we don’t provide any type of consultancy so we are sorry for being unable to reply to consultancy queries. Also, we do mention that our replies are solely on a practical basis and we advise you to cross verify with professional authorities for a fact check.”