Gujarat GST AAR Allows ITC on Input Services for Structural Supports of Plant & Machinery | Biz Flow Kit

The Gujarat-based Authority for Advance Ruling (AAR) recently delivered a very important decision clarifying that businesses can definitely claim Input Tax Credit (ITC) under the Goods and Services Tax (GST) framework for the input services utilised in building structural supports for plant and machinery installed right inside their factory premises.

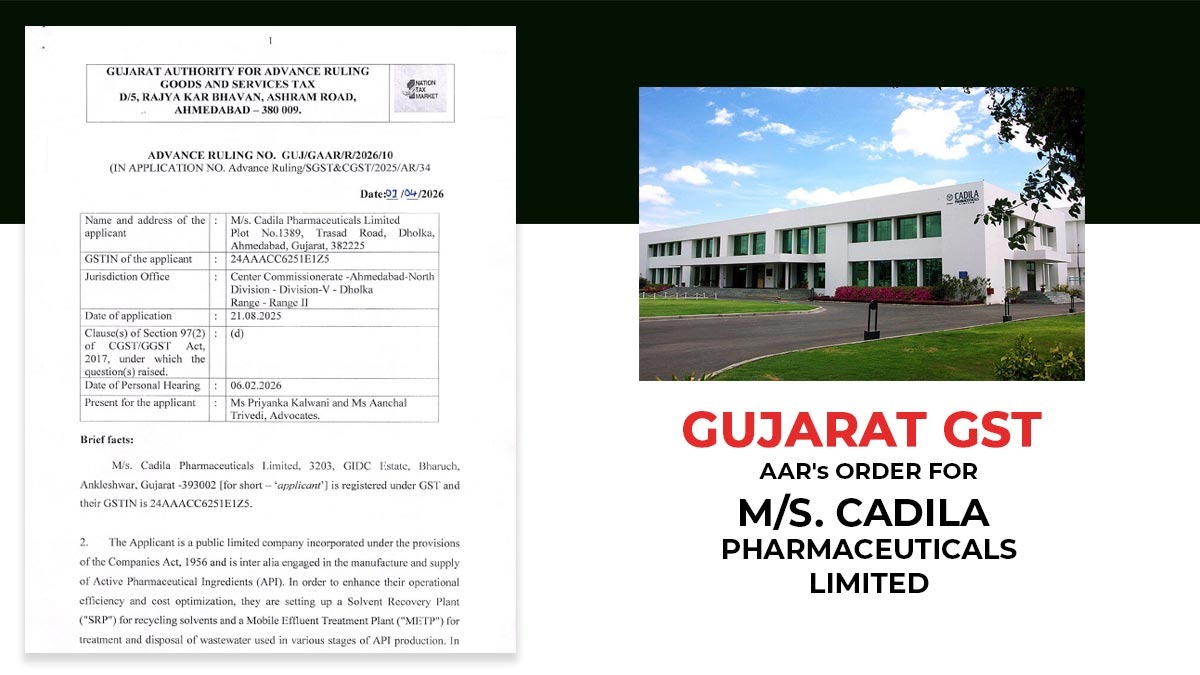

This specific case was brought forward by the applicant, M/s. Cadila Pharmaceuticals Limited. They are a well-known public limited company primarily focused on the manufacture and supply of Active Pharmaceutical Ingredients (API).

Read Also: Gujarat GST AAR: ITC on Employer-Provided Canteen Services (Excluding Employee Contribution)

Currently, the company is in the process of establishing a new Solvent Recovery Plant (SRP). The main purpose of this facility is to efficiently reclaim valuable solvents from various waste streams, which not only allows for their reuse but also significantly brings down the overall environmental impact of the company’s operations.

To get this SRP plant fully operational, several heavy-duty pieces of equipment need to be installed inside. This includes crucial items like a reactor, phase separators, heat exchangers, centrifugal pumps, a water chiller, and large cooling towers.

Because of the intense operational load, heavy torque, and strong vibrations that are naturally generated when these machines are in constant use, they simply cannot be placed flat on bare land. Instead, building a highly specialised, specifically engineered foundation is an absolute necessity before any installation can even begin.

Important: GST: Impact of New Taxation Structure on Works Contract

The vendors and suppliers who provided the necessary materials for this heavy construction issued proper tax invoices to the applicant to recover their consideration for building the structural support.

On these invoices, they properly discharged the applicable GST at a standard rate of 18%. In turn, the applicant went ahead and availed a proportionate ITC on these specific input services related to the various equipment being installed at the SRP.

The primary legal question that was presented before the AAR was quite straightforward: Is the applicant actually permitted by law to avail ITC on these specific input services? From the applicant’s perspective, they strongly believed that they are entirely eligible to claim this credit according to the provisions laid out in Section 16 of the CGST Act, 2017.

After carefully reviewing the facts, the AAR formulated the opinion that the diverse range of equipment being set up in the SRP clearly qualifies as machinery.

Consequently, it securely falls under the legal ambit of ‘plant and machinery’ as defined in the Explanation to Section 17.

Because of this classification, the ruling bench, which consisted of Sushma Vora (SGST Member) and Vishal Malani (CGST Member), formally held that the input tax credit (ITC) would indeed be fully available on the construction of the foundation and structural supports.

Read Also: How GST Software Handles Input Tax Credit (ITC) Tracking

| Case Title | M/s. Cadila Pharmaceuticals Limited |

| GSTIN of the applicant | 24AAACC6251E1Z5 |

| Date | 01.04.2026 |

| Present for the Applicant | Ms Priyanka Kalwani and Ms Aanchal Trivedi |

| Gujarat GST AAR | Read Order |