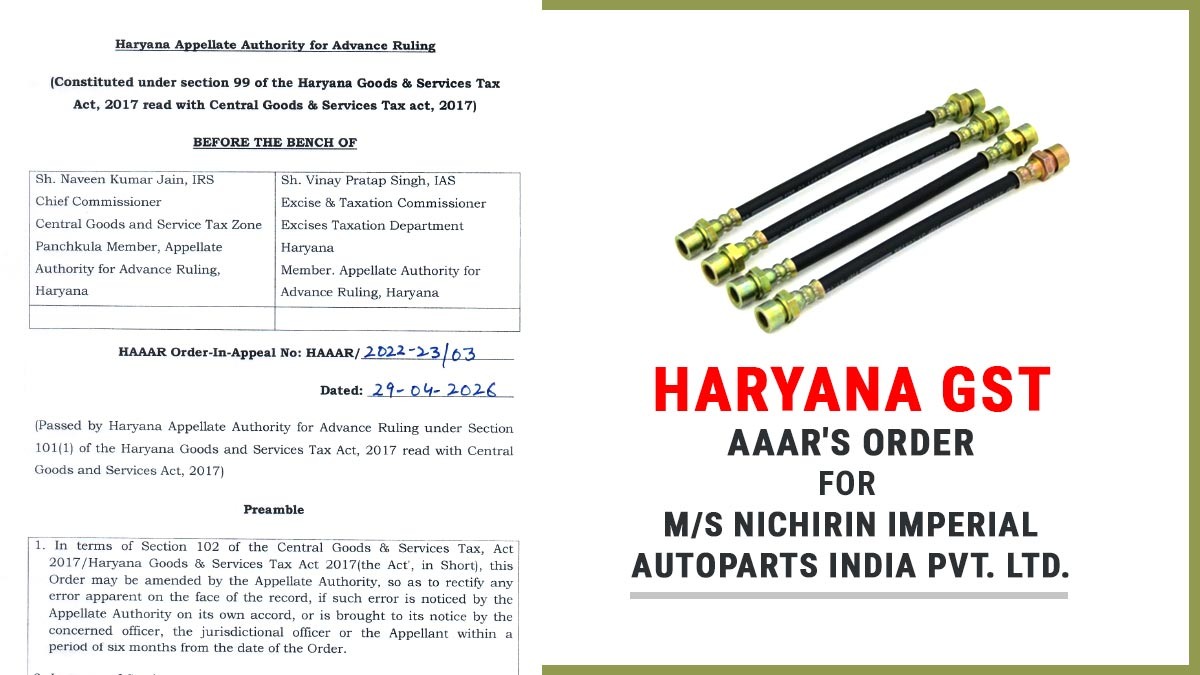

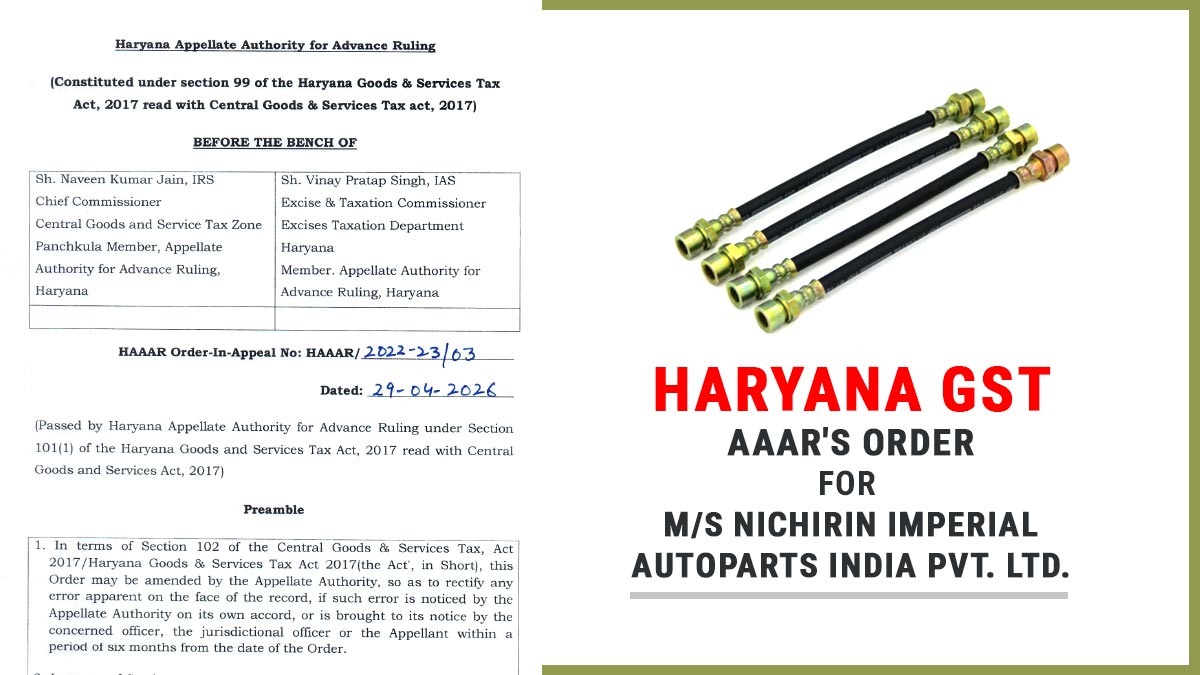

Haryana AAAR Defines Brake Hoses Under HSN 4009 and Applies 18% GST | Biz Flow Kit

The present appeal has been filed by Nichirin Imperial Autoparts India Private Limited, Faridabad, Haryana (Appellant), before the AAAR Haryana under Section 100(1) of the CGST Act, 2017 and the Haryana Goods and Services Tax Act, 2017, challenging the earlier ruling passed by the Authority for Advance Ruling (AAR), Haryana vide Order No. HR/ARL/09/2021-22 dated December 13, 2021.

The business of the appellant company is the manufacture and import of automotive components, including Brake Hoses for two-wheelers and four-wheelers.

An application has been filed by the appellant on April 15, 2022, seeking condonation of delay, as the present appeal was submitted 7 days after the time limit prescribed u/s 100(2) of the Act. The appellant then sought an Authority for Advance Ruling (AAR) from the Haryana Authority to clarify the classification and applicable GST rate for its product, i.e., “Brake Hoses”.

The AAR Haryana, post analysing the manufactured product via the appellant, categorises Brake Hoses under HSN 8708 with a GST rate of 28% for four-wheelers and under HSN 8714 with a GST rate of 5% for two-wheelers.

Read Also: GST Rates Applicable to Cars and Their Accessories

The dissatisfied appellant with the ruling of the AAR Haryana, afterwards approached the present AAAR Haryana, contesting it u/s 100 of the Haryana Goods and Services Tax Act, 2017. The appellant prayed the AAAR to set aside the ruling of the AAR Haryana, with effect from the order date.

The appellant questioned, seeking the Authority for Advance Ruling (AAR), Haryana:

- Question 1: The HSN Classification of the product, i.e., “The Break Hose”

- Question 2: GST Rate applicability for the product, i.e., “The Break Hose”, used as Four Wheeler Brake Hose and Two Wheeler Brake Hose.

Post analysing the case of the appellant, the Appellate Authority for Advance Ruling (AAAR) Haryana, decided to set aside the Authority for Advance Ruling (AAR) No. HR/ARI/09/2021-22, dated December 13, 2021, and held the product manufactured by the appellant, i.e., “Brake Hose”, is utlised as a part of braking systems in four-wheelers and two-wheelers, which, as per the GST law, must be categorized under Heading 4009 – “Tubes, pipes and hoses, of vulcanised rubber other than hard rubber, with or without their fittings (for example, joints, elbows and flanges)”. Therefore, 18% GST is chargeable on it.

Subsequently, the appeal of Nichirin Imperial Autoparts India Private Limited, Faridabad, Haryana, has been permitted.

Also Read: Revised GST Slab Rates in India

The above-mentioned ruling has been furnished via the AAAR Haryana u/s 101(1) of the Haryana Goods and Services Tax Act, 2017, read with the Central Goods and Services Act, 2017.

| Name of the Appellant | M/s Nichirin Imperial Autoparts India Pvt. Ltd. |

| GSTIN | 06AADCN4303K1ZN |

| Order No. | HAAAR/2022-23/03 |

| Represented by | Varun Khurana, Shivam Mehta |

| Haryana AAAR | Read Order |