ITAT Remands Section 80GGC Deduction Dispute to AO for Fresh Verification of Political Donation Alleged as Bogus | Biz Flow Kit

ITAT Remands Section 80GGC Deduction Dispute to AO for Fresh Verification of Political Donation Alleged as Bogus

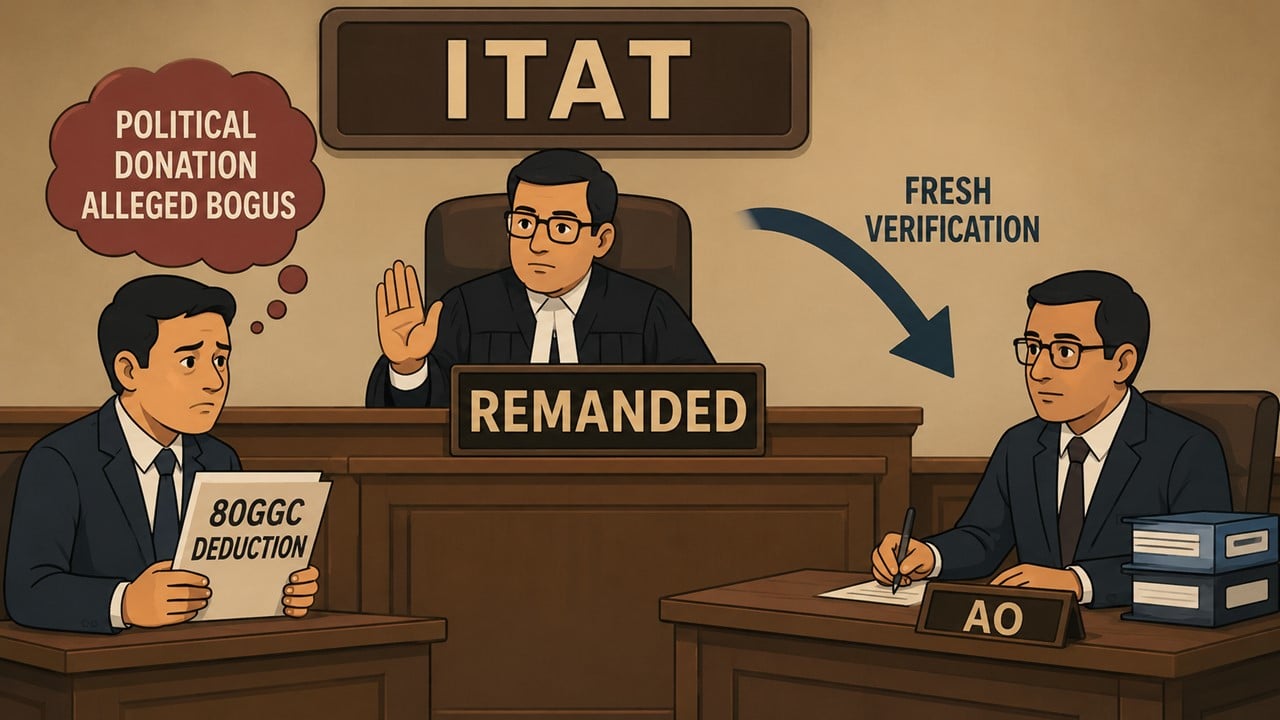

The Ahmedabad Bench of the Income Tax Appellate Tribunal (ITAT) has partly allowed the appeal of Mr. Sureshkumar Prahladbhai Patel for Assessment Year 2019-20 and has sent the matter back to the AO for fresh examination.

The dispute is in relation to the donation of Rs 2,51,000 made by the assessee to Yuva Janjagriti Party for which deduction was claimed under Section 80GGC of the Income Tax Act. During the search on some registered but unrecognised political parties, the Income Tax Department allegedly found that some parties were issuing receipts of donations and then returning the amount donated in cash after deducting commission. The department on the basis of this information reopened the case of the assessee under section 147.

The AO disallowed the deduction of Rs 2,51,000 on the ground that the donation was not genuine. The CIT(A) also confirmed the addition.

The assessee before the Tribunal claimed that the donation was genuine and was made through banking channels. The assessee submitted the donation receipt, bank statement, PAN details of the political party, income tax return and computation of income in support of the claim. It was contended that there was no involvement in any bogus transaction.

The Tribunal first examined the validity of the reopening of assessment. It observed that the reopening was justified because the department had received specific information from the search proceedings, and the assessee himself had admitted making the donation to the political party. Therefore, the challenge against the reopening was rejected.

On the merits of the addition, however, the Tribunal noted that the Assessing Officer had not properly verified the bank statements. According to the Tribunal, it was necessary to examine whether the assessee had received back the donated amount in cash or through any other means, and whether there were any related cash transactions before or after the donation.

Since these crucial facts had not been adequately verified, the Tribunal set aside the issue and remanded the matter to the Assessing Officer for fresh verification and a decision on merits. The AO has been directed to provide the assessee with a proper opportunity of being heard and to follow the principles of natural justice.

As a result, the appeal was partly allowed for statistical purposes.

Join StudyCafe Membership. For More details about Membership Click Join Membership Button

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe’s WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!”

![Govt bars vehicle to get more than 200 Litre Diesel [Read Notification]](https://bizflowkit.in/wp-content/uploads/2026/06/Centre-Restricts-Bulk-Diesel-Purchases-at-Petrol-Pumps-Amid-Global-Fuel-Supply-Concerns-768x432.jpg)