Punjab & Haryana HC Rules PLC Not Separately Taxable Under GST | Biz Flow Kit

In this situation, a real estate developer sought guidance from the Advance Ruling Authority regarding a specific question. They wanted to know if the extra fees charged to buyers for selecting the location of their flats, known as Preferential Location Charges (PLC), should be taxed on their own or included with the main charges for construction or development services.

On August 28, 2020, the Advance Ruling Authority ruled that PLC constitutes an independent supply and is subject to separate taxation from construction services. The appellate authority upheld this ruling on March 28, 2022, u/s 101 of the CGST Act.

Thereafter, in the 54th meeting conducted on 09.09.2024, the GST council suggested that preferential location charges collected by developers must not be charged to tax separately, because these charges create an integral part of construction services. As per the suggestion, the Government of India issued a clarification on 11.10.2024 u/s 168(1) of the CGST Act, citing that PLC forms part of a composite supply where construction service is the principal supply and thus draws GST on an identical rate as applicable to construction services before issuance of the completion certificate.

Read Also: Current GST Rate and HSN Code on Construction Services

The question at hand is whether the Preferential Location Charges (PLC) that a developer collects for allotting flats in preferred locations should be considered a separate taxable supply or included as part of the composite supply of construction services, which is taxed at the same rate as the main construction service.

The High Court affirmed that the issued clarification from the Government of India u/s 168(1) of the CGST Act, founded on the suggestions of the GST Council, was binding upon the departmental authorities. The Court noted that the circular unquestionably stated that the choice of location is an integral part of construction service, and PLC is naturally bundled with such supply. Therefore, no tax is to be imposed on PLC independent of construction services.

The Court determined that the circular, being clarificatory in nature, would apply retrospectively. As a result, the orders of the Advance Ruling Authority and the appellate authority, which stated that PLC was independently taxable, were inconsistent with the clarification issued later and, therefore, should be quashed.

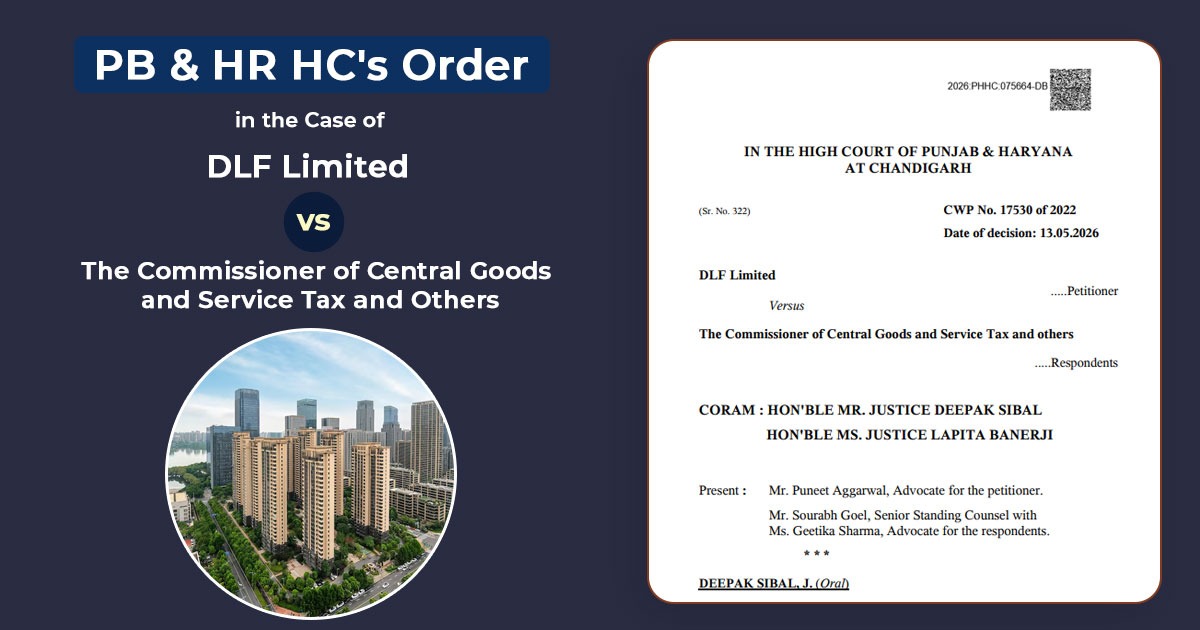

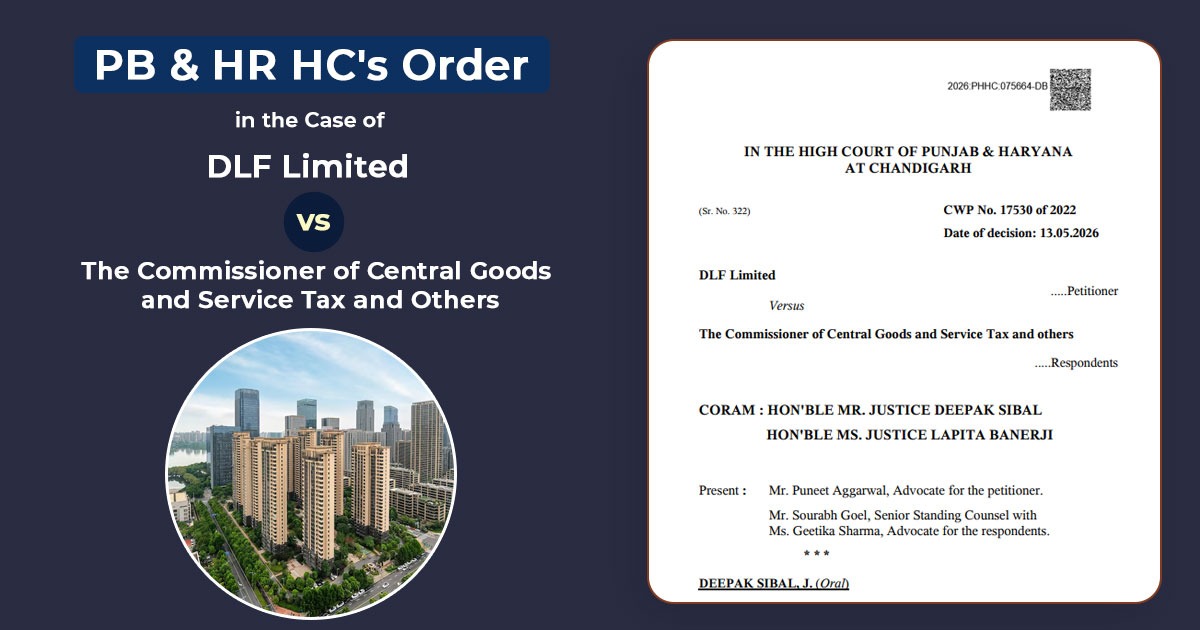

| Case Title | DLF Limited Versus The Commissioner of Central Goods and Service Tax and Others |

| Case No. | CWP No. 17530 of 2022 |

| For Petitioner | Mr. Puneet Aggarwal, Advocate |

| For Respondent | Mr. Sourabh Goel, Senior Standing Counsel with Ms. Geetika Sharma, Advocate |

| Punjab and Haryana High Court | Read Order |