TDS and TCS Compliance Calendar July 2026 | Biz Flow Kit

Introduction

The TDS and TCS Compliance Calendar July 2026 is a comprehensive guide for businesses, employers, and tax deductors to track important due dates for tax deduction and collection. It includes deadlines for TDS/TCS return filing, tax payment, and issuing certificates for the relevant quarter.

Following this calendar helps taxpayers stay compliant under the Income Tax Act, 2025, while avoiding late fees, penalties, and filing errors.

Important dates in the TDS and TCS Compliance Calendar July 2026

|

Due Date |

Compliance |

Form |

Period |

Applicable To |

|

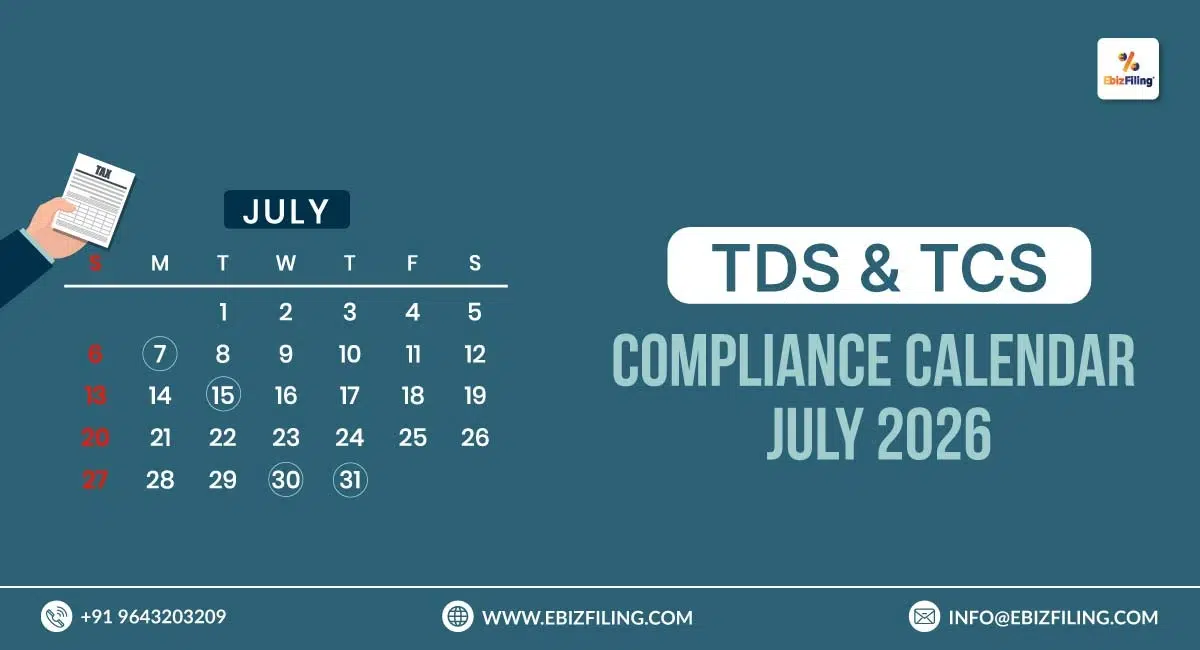

07/07/2026 |

Deposit of TDS/TCS deducted or collected | Challan ITNS 281 | June 2026 | All Deductors and Collectors |

| 15/07/2026 | Quarterly TCS Return Filing | Form 143 | April–June 2026 Quarter |

TCS Collectors |

|

30/07/2026 |

Issue of TCS Certificate | Form 148 | April–June 2026 Quarter | TCS Collectors |

| 31/07/2026 | Quarterly TDS Return Filing (Salary) | Form 138 | April–June 2026 Quarter |

Employers |

|

31/07/2026 |

Quarterly TDS Return Filing (Non-Salary Payments to Residents) | Form 140 | April–June 2026 Quarter | Deductors |

| 31/07/2026 | Quarterly TDS Return Filing (Specified Payments) | Form 144 | April–June 2026 Quarter |

Applicable Deductors |

Disclaimer: The above form numbers reflect the new numbering framework introduced under the Income Tax Act, 2025. Under the Income Tax Act, 2025, Form 24Q has been replaced by Form 138, Form 26Q by Form 140, Form 27EQ by Form 143, Form 27Q by Form 144, and Form 27D by Form 148.

Penalties Under the Income Tax Act, 2025 (TDS and TCS Compliance Calendar July 2026)

|

Default Type |

Relevant Provision |

Penalty / Consequence |

Remarks |

|

Late filing of TDS/TCS return (Forms 138/140/143/144 etc.) |

Section on late filing fee | ₹200 per day of delay (till filing) | Maximum up to TDS/TCS amount of the quarter |

| Failure to file / incorrect TDS/TCS return | Penalty provision for inaccurate/non-filing | ₹10,000 to ₹1,00,000 |

Applies even if tax is deposited |

|

Failure to deduct or collect TDS/TCS |

Deduction/collection default provisions | Penalty equal to tax not deducted/collected | Can trigger demand + compliance action |

| Delay in deposit of TDS/TCS | Interest provisions | 1% per month for failure to deduct tax and 1.5% per month for failure to deposit tax after deduction, as applicable. |

Charged till date of payment |

|

Wilful default / serious non-compliance |

Prosecution provisions | Imprisonment: 3 months to 7 years + fine |

Applicable in severe or repeated defaults |

Disclaimer: This table is based on the provisions of the Income Tax Act, 2025, effective from 1 April 2026.

How Ebizfiling Can Help You Stay Compliant?

Keeping track of deadlines under the TDS and TCS Compliance Calendar July 2026 can be challenging for businesses, especially when managing multiple responsibilities such as GST, income tax, ROC, PF, and ESI compliance requirements simultaneously. Missing even one due date can lead to penalties, interest, and unnecessary compliance notices.

Ebizfiling makes this process simple by providing expert support for timely filings, accurate reporting, and complete compliance management. Whether it is return preparation, documentation, or deadline tracking, we ensure everything is handled smoothly and on time.

Get expert assistance for TDS return filing with Ebizfiling and stay stress-free about your compliance obligations.

Conclusion

Following the TDS and TCS Compliance Calendar July 2026 is essential to ensure timely completion of all TDS and TCS obligations. Timely filing and payment help avoid penalties, interest, and other compliance-related issues.

It also ensures smooth tax credit for deductees and helps businesses maintain effective compliance management.

You can also refer to our complete Compliance Calendar July 2026 for all GST, TDS/TCS, Income Tax, PF, ESI, LLP, and company compliance due dates in one place.

Suggested Reads:

TDS and TCS Compliance Calendar June 2026

GST compliance Calendar July 2026

Income Tax Compliance Calendar July 2026

PF and ESI Compliance Calendar July 2026

Frequently Asked Questions

1. What happens if TDS or TCS is not deposited within the prescribed due date?

Failure to deposit TDS or TCS within the prescribed due date attracts interest liability under the Income-tax Act, 2025. Delayed payment may also result in penalties, notices from the Income Tax Department, and prosecution proceedings in serious cases. Additionally, non-compliance may affect the deductor’s ability to claim certain business expenditures. TDS and TCS payments are reported through statements filed under Sections 397 and 394, respectively.

2. What interest is applicable for delayed deposit of TDS?

If tax is deducted but not deposited on time, interest is payable at 1.5% per month or part thereof from the date of deduction to the date of actual payment. If tax was not deducted when required, interest is charged at 1% per month or part thereof from the date on which the tax was deductible until the date of actual deduction. These provisions continue under the Income-tax Act, 2025.

3. What are the late filing fees for delayed submission of TDS or TCS returns?

Under Section 427 of the Income-tax Act, 2025, a late filing fee of ₹200 per day is levied for delayed filing of TDS or TCS statements. The total fee cannot exceed the amount of TDS deducted or TCS collected for the relevant period. The fee must be paid before filing the delayed statement.

4. What penalties can be imposed for non-filing or incorrect filing of TDS or TCS returns?

In addition to the late filing fee under Section 427, the Assessing Officer may levy a penalty under Section 461 ranging from ₹10,000 to ₹1,00,000 for failure to furnish TDS or TCS statements within the prescribed time or for furnishing incorrect information.

5. What happens if incorrect details are reported in a TDS or TCS return?

Incorrect reporting of PAN, challan details, deduction amounts, or deductee information may result in mismatches in the tax credit statement, denial of tax credit to the deductee, and issuance of notices by the Income Tax Department. Such errors should be rectified promptly by filing a correction statement through the applicable portal.

6. Can a TDS or TCS return be revised after filing?

Yes. A correction statement can be filed to rectify errors in the original TDS or TCS return, including incorrect PAN, challan details, deduction amounts, and deductee information. For Tax Year 2026-27 onwards, TDS and TCS statements are filed under Section 397(3)(b) of the Income-tax Act, 2025.

7. Can expenditure be disallowed if TDS is not deducted or deposited on time?

Yes. Under the Income-tax Act, 2025, certain business expenditures may be disallowed if TDS is not deducted or, after deduction, is not deposited within the prescribed timelines. This increases the taxable income of the deductor and results in additional tax liability.

8. What are the prosecution provisions for failure to deposit TDS with the government?

Failure to deposit TDS after deduction may attract prosecution under Section 480 of the Income-tax Act, 2025. The person responsible may face rigorous imprisonment ranging from three months to seven years, along with a fine, depending on the nature and severity of the default.

9. How can businesses streamline TDS and TCS compliance with Ebizfiling?

Businesses can simplify TDS and TCS compliance with Ebizfiling by obtaining support for tax applicability analysis, tax deposits, quarterly statement filing, correction statements, due date tracking, and notice management.

10. Does Ebizfiling assist with TDS/TCS return corrections and compliance notices?

Yes. Ebizfiling provides end-to-end assistance for filing revised TDS and TCS statements, resolving defaults, responding to notices, and ensuring timely compliance under the Income-tax Act, 2025.