Karnataka HC Quashes GST Order Over ITC Mismatch Between GSTR-3B and GSTR-2A | Biz Flow Kit

The Karnataka High Court has allowed a company to reconcile the mismatches between the ITC claimed in its GSTR-3B returns and the data shown in GSTR-2A.

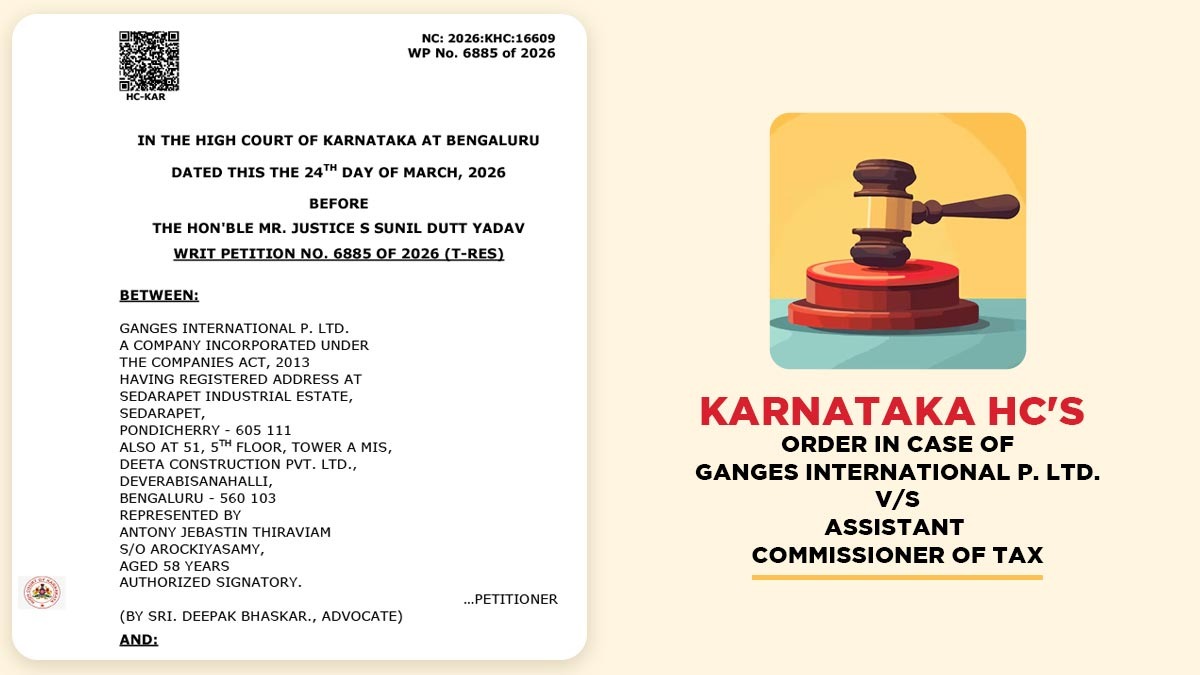

The company, Ganges International Pvt. Ltd had contested the order of the tax authority that raised a demand for an incorrectly claimed ITC under GST.

The various issues are raised by the tax authority, such as excess ITC claimed, ITC claimed on invoices from non-existent suppliers, and non-payment of GST under the Reverse Charge Mechanism (RCM). As per such findings, the authority had issued a demand, citing that the company had claimed ineligible ITC.

As per the company, if there were mismatches between the ITC claimed in Form GSTR-3B and the details in Form GSTR-2A, the authority must comply with the process cited in Circular No.183/15/2022-GST issued on 27th December 2022.

The same circular furnishes clarification for the circumstances where there are mismatches between the ITC claimed in their GSTR-3B returns and the data shown in GSTR-2A.

The HC agreed with the company that the same process had not been complied with. The court mentioned that all mismatches between the ITC claimed in Form GSTR-3B and the details in Form GSTR-2A must be authorised to be reconciled within the circular.

Also Read: How GST Software Handles Input Tax Credit (ITC) Tracking

Hence, the court set aside the order and sent the case back to the tax authorities for fresh consideration.

| Case Title | Ganges International P. Ltd. Vs. Assistant Commissioner of Tax |

| Case No. | Writ Petition No. 6885 of 2026 (T-Res) |

| For Petitioner | Deepak Bhaskar |

| For Respondent | Aravind V Chavan |

| Karnataka High Court | Read Order |

Disclaimer:- “All the information given is from credible and authentic resources and has been published after moderation. Any change in detail or information other than fact must be considered a human error. The blog we write is to provide updated information. You can raise any query on matters related to blog content. Also, note that we don’t provide any type of consultancy so we are sorry for being unable to reply to consultancy queries. Also, we do mention that our replies are solely on a practical basis and we advise you to cross verify with professional authorities for a fact check.”